Full year 2025 and Q4 2025 results

Press Release

Haaksbergen, the Netherlands

5 Mar 2026

TKH delivers strong Q4

Highlights fourth quarter 2025

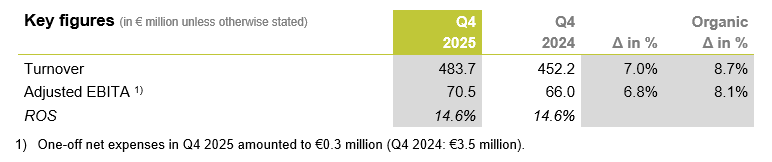

Turnover increased by 8.7% organically to €483.7 million

Added value of 52.4%

Adjusted EBITA increased by 8.1% organically to €70.5 million with a substantial improvement at Electrification

ROS at 14.6%

Highlights FY 2025

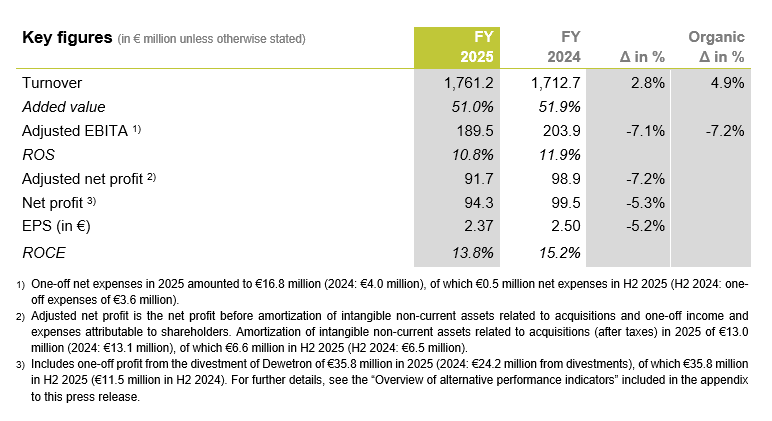

Turnover increased by 4.9% organically to €1,761.2 million

Added value of 51.0%

Adjusted EBITA decreased by 7.2% organically to €189.5 million

ROS at 10.8%

Order intake of €1,661.4 million, resulting in order book of €1,027.8 million

Innovation at 17.0% of turnover

Proposed dividend of €1.35 for 2025

Sharpened strategic focus on core activities; separation of Electrification in progress

Outlook 2026

For 2026, we anticipate organic growth in turnover and Adjusted EBITA, with a weak first quarter

Alexander van der Lof, CEO of technology company TKH: “In line with expectations, we delivered a strong Q4 2025, driven by continued solid performance in Automation and a substantial improvement in Electrification. Within Automation, Vision Technologies performed strongly throughout the year, benefiting from our differentiated and innovative technologies, our focus on providing integrated solutions and our global footprint. Turnover in Automated Machinery was impacted by softer order intake, albeit with lesser impact than initially expected. The growth drivers for Automation remain very strong, on the back of the increasing need for automated hands-off, eyes-off production.

Within Electrification, we have solved the main challenges related to the ramp‑up of our new subsea cable facility in Eemshaven. While our results in 2025 were significantly impacted, the production output of offshore inter-array cables gradually increased throughout the year. The type approval tests for larger dimensions were successfully completed during the year. The ramp-up of the larger dimensions in Q4 took longer than anticipated, limiting output. To improve operational output of larger dimensions, a necessary upgrade to a key production line has recently been successfully implemented. The advanced design and production technology of our subsea cables has resulted in a win rate of over 80% and a solid order book underlining the competitiveness of our proposition. In addition, the onshore energy market continues to show strong structural demand, with a large framework contract recently awarded to TKH.

During 2025, we made further progress in sharpening our focus on our core activities. We divested Dewetron in October, generating a one-off profit contribution of €35.8 million. In total, we divested €458 million in turnover since 2019. We remain committed to further portfolio optimization, including the intended divestment of Digitalization, in line with our “Capitalize & Execute 2028” strategy presented at our Capital Markets Day in September 2025.

As we enter 2026, we are actively preparing for the intended separation of Electrification and Automation, with TKH’s future focus on Automation. We will run a dual-track process to unlock the value of Electrification, bearing the interests of all stakeholders in mind. This will further sharpen our strategic profile and support sustainable long-term value creation. We are excited about the promising opportunities ahead for TKH, as we continue to build on our unique technologies and our leading market positions.”

ESG

Throughout 2025, we continued to strengthen our sustainability performance. We made further progress on our ESG agenda, including reducing our carbon footprint in scopes 1 and 2 to 76.3% compared to 2019. The CDP ESG-rating of TKH has been improved from B to A-, confirming our environmental leadership. We achieved EcoVadis Gold awards for our largest operations in Automation and Electrification, which means a top-5% position of all globally participating companies. The share of turnover linked to United Nations Sustainable Development Goals (SDGs) increased from 71.6% to 75.3%. We also set a new target to reduce our water‑intensity ratio by an average of 5% per year from 2026 to 2030. As part of our Capital Markets Day 2028 targets, we raised our safety, employee satisfaction and customer satisfaction targets after outperforming the previous benchmark in 2024.

Dividend proposal

The 2026 General Meeting of Shareholders will be asked to approve the payment of a 2025 cash dividend of €1.35 per (depositary receipt for a) share (2024: €1.50), representing a payout ratio of 58.7% of the net profit before amortization and one-off income and expenses attributable to shareholders (2024: 60.5%) and 57.1% of the net profit attributable to shareholders (2024: 60.0%). The dividend will be payable on June 2, 2026.

Financial developments fourth quarter 2025

In the fourth quarter of 2025, turnover increased organically by 8.7% and Adjusted EBITA by 8.1% compared to Q4 2024 reflecting higher output levels. Electrification recorded strong organic turnover growth of 29.0%, driven by increased output levels of offshore inter-array cables at the Eemshaven factory and continued strong demand in onshore energy. Turnover at Vision Technologies grew by 1.8%, against a strong comparison base in Q4 2024. As expected, Automated Machinery’s turnover declined by 6.9% organically, reflecting lower order intake earlier in the year. The Adjusted EBITA of Electrification increased very strongly, benefiting from higher turnover and improving yields. Moreover, the excellent operational performance of projects nearing completion in Tire Building systems had a positive impact in Q4 2025. ROS reached 14.6% for the quarter.

Financial developments full year 2025

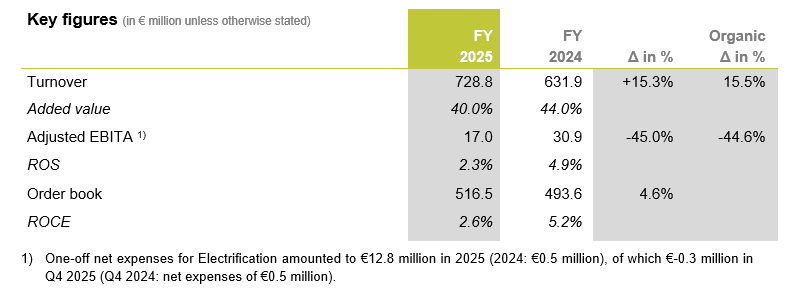

Turnover reached €1,761.2 million in 2025, representing organic growth of 4.9% (2024: €1,712.7 million), with Electrification (Smart Connectivity systems) showing the highest organic growth rate at 15.5%. Vision Technologies (Smart Vision systems) recorded organic turnover growth of 6.7%, while Automated Machinery (Smart Manufacturing systems) declined by 8.6%. Acquisitions accounted for +0.4% and divestments accounted for -1.9% of total turnover.

The order intake in 2025 amounted to €1,661.4 million (2024: €1,911.4 million), resulting in an order book of €1,027.8 million at year-end (2024 €1,135.0 million). As expected, the order book at Automated Machinery declined to €380.9 million at year-end 2025 (2024: €501.5 million), reflecting lower intake from Tier 1 customers and ongoing geopolitical uncertainty. Vision Technologies also reported declines in their order book of 6.7% partly due to the progress made on large projects. In Electrification, the order book grew with 4.6% due to the winning of new contracts for offshore inter-array cables.

Added value reached 51.0% in 2025 (2024: 51.9%), with added value in both Automated Machinery and Vision Technologies increasing to 54.3% (2024: 51.5%) and 62.0% (2024: 60.6%), respectively. Added value at Electrification declined to 40.0% (2024: 44.0%), due to a higher share of outsourced services in the sales mix.

Operating expenses (excluding one-off income and expenses, amortization, and impairments) increased by 3.6% year over year, mainly due to higher depreciation costs resulting from the commissioning of the strategic capex program. As a result, Adjusted EBITA decreased organically by 7.2% to €189.5 million in 2025. ROS decreased to 10.8% (2024: 11.9%), impacted by lower yields, and the ramp-up and start-up costs at the Eemshaven facility.

In 2025, one-off expenses at EBITA level amounted to €16.8 million (2024: €4.0 million), related to acquisitions and divestments, one-off transportation costs due to the delayed ramp-up of Eemshaven, and restructuring costs, primarily within the Telecom activities.

Amortization increased slightly to €61.0 million (2024: €60.8 million) due to the higher amortization of capitalized R&D. Impairments amounted to €8.7 million (2024: €8.5 million), mainly related to underutilized right-of-use and fibre optic network assets.

Net financial expenses decreased to €28.4 million (2024: €29.3 million), reflecting lower average interest rates. The results from associates and subsidiaries amounted to €34.2 million (2024: €24.5 million) including the one-off profit from the divestment of Dewetron of €35.8 million (2024: divestment of HE System Electronic and EKB Groep of €24.6 million).

The normalized effective tax rate decreased to 22.1% in 2025 (2024: 24.4%) partly due to R&D tax facilities in several countries.

Net profit before amortization of intangible non-current assets related to acquisitions and one-off income and expenses attributable to shareholders decreased by 7.2% to €91.7 million (2024: €98.9 million). Net profit decreased to €94.3 million (2024: €99.5 million). Earnings per share before amortization, one-off income, and expenses amounted to €2.30 (2024: €2.48). Ordinary earnings per share were €2.37 (2024: €2.50).

Net bank debt according to bank covenants decreased from €496.0 million at year-end 2024 to €461.4 million at year-end 2025. The main items affecting the debt level include net investments in property, plant, and equipment of €69.0 million (2024: €98.7 million, including €49.0 million related to the strategic investment program), investments in intangible assets (€60.1 million), and dividends paid (€59.9 million). Divestments amounted to €54.2 million in 2025, including the €35.8 million one-off profit. Cash flow from operating activities amounted to €192.4 million (2024: €196.2 million). Working capital improved to 17.0% of turnover (2024: 17.9%). The net debt/EBITDA ratio, calculated according to TKH’s bank covenant, was 1.9, well within the financial ratio agreed with our banks. Solvency improved to 41.8% (2024: 39.9%).

At year-end 2025, TKH employed a total of 6,759 FTEs (2024: 6,640), including 455 temporary employees (2024: 351 FTEs).

Developments per segment

AUTOMATION

In Automation, we aim to be a global market leader in Vision Technologies and Automated Machinery, enhancing Automation through state-of-the-art AI-integrated solutions.

Vision Technologies (Smart Vision systems)

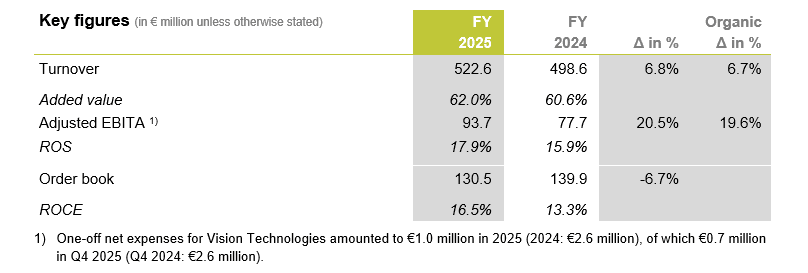

In 2025, turnover in Vision Technologies increased by 6.7% organically to €522.6 million. Added value improved to 62.0%, up from 60.6% in 2024, reflecting the differentiated and high-margin nature of our vision portfolio. Operating leverage from higher turnover, combined with realized cost savings, resulted in strong organic growth of 19.6% in Adjusted EBITA and a ROS of 17.9%

Vision Technology (88% of segment turnover) – Growth in 2025 was mainly driven by Machine Vision. In 2D Machine Vision, growth was achieved in the United States and Asia-Pacific across most end markets, while Europe, in particular Germany, remained challenging. Further progress was made in the defense sector, in particular in situational awareness applications. During the year, we consolidated our 2D Vision brands under the Allied Vision brand. The unified brand structure supports increasing demand for integrated solutions and enhances our one-stop-shop proposition. With a strong focus on solutions and software, 3D Machine Vision secured project wins in battery manufacturing and consumer electronics, mainly in Asia, and achieved growth in factory automation and wood processing in the Americas. Vision solutions for vision-guided robotics in material handling and automotive applications also recorded continued growth.

Security Vision recorded modest growth, supported by the demand for high end mission critical systems. Furthermore, the delivery of automated parking guidance systems, with camera-based smart sensors in the United States, combining efficiency and security functionalities also contributed to the growth in turnover.

Automated Machinery (Smart Manufacturing systems)

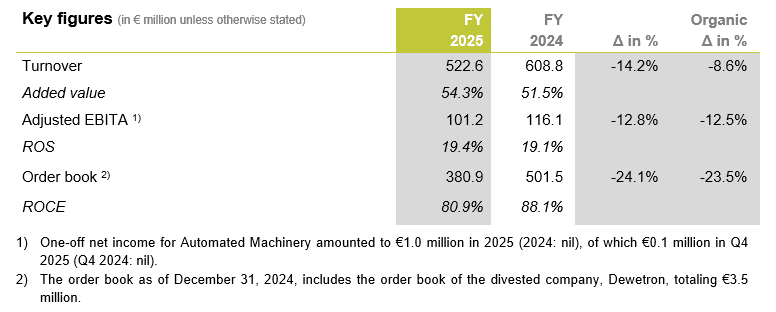

In line with expectations, turnover at Automated Machinery declined organically by 8.6% in 2025, reflecting a strong comparison base with 2024 and lower order intake in tire building systems during the year. The divestment of Dewetron (2024 turnover of €29.4 million) accounted for 5.4% of the reported turnover decline. The order book decreased organically by 23.5% year on year to €380.9 million, primarily due to lower order intake from Tier 1 customers. Ongoing geopolitical uncertainty also delayed order placements by Tier 2 and Tier 3 customers. Added value increased further to 54.3% (from 51.5% previously), driven by an improved product mix and continued efficiency improvements. The excellent operational performance on projects nearing completion in Tire Building systems had a positive impact in Q4 2025. Adjusted EBITA was down organically by 12.5% to €101.2 million, while ROS improved to 19.4%.

In 2025, the first full UNIXX platform was successfully delivered, with repeat orders subsequently secured. We also secured the first order for UNIXX Moto, expanding the platform into radial motorcycle tires assembly. Service revenues continued to grow, further supporting margin resilience. The structural drivers for tire building systems remain very strong, as the need for greater production flexibility, increased sustainability demands, and higher levels of automation will fuel future demand for more advanced tire building systems.

ELECTRIFICATION

The Electrification segment consists of connectivity systems for onshore and offshore activities, with unique technologies and a strong sustainability and service offering.

Electrification (Smart Connectivity systems)

Turnover in this segment increased organically by 15.5% to €728.8 million in 2025. Added value as a percentage of turnover decreased from 44.0% to 40.0% in 2025, partly due to a higher share of outsourced services in offshore energy. Adjusted EBITA decreased organically by 44.6% to €17.0 million, mainly due to lower production output and yields during the ramp-up of the Eemshaven facility, as well as continued weakness in Digitalization. In Q4 2025, there was a marked improvement in Electrification results, with turnover growing by 29.0% and a very strong growth of Adjusted EBITA. ROS amounted to 2.3% for 2025. The order book increased to €516.5 million due to the winning of new contracts for offshore inter-array cables.

Electrification (72% of segment turnover) – In Q4 2025, Electrification delivered strong turnover growth. Offshore energy benefited from the contribution from outsourced services and accessories. The ramp‑up of the new subsea cable facility in Eemshaven encountered output challenges, impacting results in 2025. These technical issues were gradually resolved during the year, with production output of offshore inter-array cables increasing. Significant upgrades to production processes were made and type approval tests for larger dimensions were successfully completed during the year. The ramp-up of the larger dimensions in Q4 took longer than anticipated, limiting output. To improve the operational output of larger dimensions, a further necessary upgrade to a key production line has recently been successfully implemented, with continued optimization steps planned for 2026. During the year, new offshore wind contracts were signed for the supply of inter-array cables in the coming years. The sales funnel remains strong.

Onshore energy recorded turnover growth, supported by strong structural higher demand that is expected to continue in the coming years. A large, multi-year framework contract was recently signed with Distribution System Operator (‘DSO’) Alliander with a value of approximately €650 million for the coming 8 years. There are framework agreements with various DSO’s in place but not reflected in the order book. These framework agreements provide a basis for substantial growth in the years ahead.

Industrial specialty cables showed solid performance during the year, although lower than in 2024, due to the ongoing challenges in the German industrial market.

Digitalization (25% of segment turnover) – Turnover at Digitalization dropped in 2025, impacted by a significant decline in demand due to the continued low levels of investment in the rollout of fibre optic networks in Europe. Pricing pressure, combined with ramp-up costs, significantly impacted results in 2025. The consolidation of fibre optic cable manufacturing at the Polish facility has been completed, resulting in lower operating expenses from 2026 onwards.

Outlook

TKH’s strong building blocks with leading technologies and strong market positions, forms a strong foundation for 2026. Barring unforeseen circumstances, we expect on balance organic growth in turnover and Adjusted EBITA in 2026, albeit with a weak first quarter.

You can follow the presentation of the full-year results on March 5, 2026, at 10:00 CET via video webcast (www.tkhgroup.com).

Haaksbergen, March 5, 2026

For further information:

Jacqueline Lenterman

Investor Relations

j.lenterman@tkhgroup.com

Tel: +31(0)53 5732901