Full year 2024 and Q4 2024 results

Press Release

Haaksbergen, the Netherlands

4 Mar 2025

TKH delivers strong Q4

Highlights fourth quarter 2024

- Turnover increased 4.7% organically to €452.2 million, with growth in all segments; strong performance in Smart Vision and Smart Manufacturing systems

- Added value increased to 52.4%

- EBITA excluding one-off income and expenses increased 5.1% organically to €66.0 million

- ROS at 14.6%

Highlights FY 2024

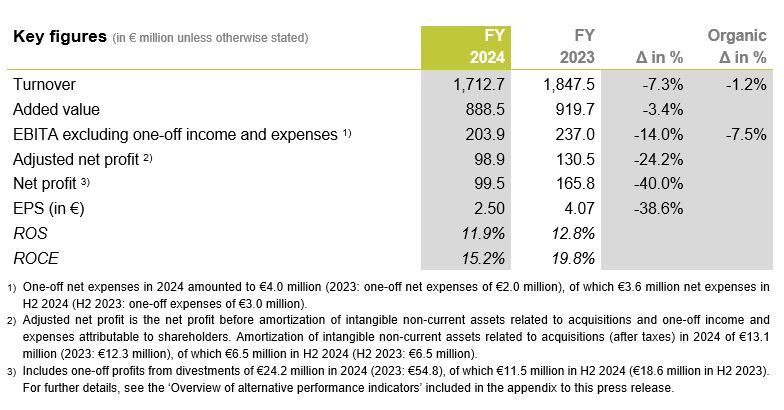

- Turnover decreased by 1.2% organically to €1,712.7 million

- Added value at 51.9%, underlining the market differentiation of our technologies

- EBITA excluding one-off income and expenses decreased by 7.5% organically to €203.9 million, in line with the outlook of €200-€210 million

- ROS at 11.9%

- Adjusted net profit of €98.9 million

- Order intake of €1,911.4 million, resulting in a record order book of €1,135.0 million

- Good progress on ESG targets, improved ratings, SDGs at 71.6% of turnover

- Innovation at 17.6% of turnover

- Dividend of €1.50 proposed for 2024

- Serial production of inter-array cables in Eemshaven expected to commence shortly

- For 2025, we anticipate organic growth in turnover and EBITA excluding one-off income and expenses, with a weak first quarter

- Strategic update leading to next phase of focus and optimization; TKH plans to host a CMD on September 25, 2025

Alexander van der Lof, CEO of technology company TKH: “With Q4 showing growth in all segments, we realized a strong end to the year. Smart Vision systems reported record results in Q4 on the back of the large orders secured earlier in the year, and the robust order book positions us for further growth. Smart Manufacturing and Smart Connectivity systems also contributed to the growth, and ROS for the group in the fourth quarter was a strong 14.6%.

During the year under review, Smart Connectivity systems showed a weak performance. The strong market headwinds in Digitalization led to a sharp decline in volumes, which we addressed by relocating all fibre optic cable production to Poland to reduce costs. In Electrification, the effects of destocking of onshore cables by the Dutch utility companies continued throughout 2024. Strong progress was made in positioning for growth in Europe. The postponement of the ramp-up of the new inter-array cable factory in Eemshaven resulted in low turnover for offshore inter-array cables and additional start-up and ramp-up costs. Good progress has been made in the past months to remove the bottlenecks enabling us to start serial production shortly.

In 2024, we concluded our €200 million investment program. We further optimized our portfolio, divesting two large non-core entities in our Smart Manufacturing segment, with a combined turnover of €56 million in 2023. We also acquired three smaller companies with state-of-the-art technologies, two of which in our automation-driven Smart Vision segment.

In 2025, we will see the full benefits of the €15 million cost-saving measures we implemented. Combined with expected growth in Smart Vision systems and strong growth in Smart Connectivity systems driven by the strong order book, we expect overall organic growth of both turnover and EBITA excluding one-off income and expenses in 2025.

As this is the last year of our Accelerate 2025 strategy, we have started to review our strategy going forward. We have achieved many of the milestones we defined for this period, but also due to geopolitical developments and resulting market headwinds, we have not realized our full potential within the timeframe. Building on our strong foundations, our strategy for the next phase will focus on Automation and Electrification as guiding global trends. Our leading positions and mature technologies on the back of our innovations and R&D roadmap, will allow us to gain further market share and expand our addressable market. In addition, a combination of cost optimizations, optimized integrations and commercial excellence programs will add to further margin expansion. As part of our strong focus on Automation and Electrification, we will implement a matching divestment program, using the proceeds to further build our core technologies, while returning any excess cash to shareholders. We plan to host a Capital Markets Day on September 25, 2025 to present our fully defined strategy and targets for the next phase.”

ESG

TKH made further progress in 2024 on its key sustainability targets as set out in the Accelerate 2025 strategic program. Our net carbon market-based footprint for scopes 1 and 2 decreased by 70.3% in 2024 compared with the reference year 2019 (2023: 64.3%). This excludes acquired carbon offsets and was mainly driven by energy efficiency measures, a higher share of renewable energy and green certificates. In 2024, the percentage of female employees in executive and senior management roles increased to 21.6% from 19.2% in 2023. The percentage of turnover related to the Sustainable Development Goals (SDGs) was 71.6% (2023: 70.2%).

Nominations for reappointments to the Supervisory Board

At the close of the AGM 2025, to be held on 15 May 2025, the term of Mr. J.M. Kroon and Mrs. C.W. Gorter as member of the Supervisory Board will expire, in accordance with the applicable schedule of retirement. Under the regulations of the Supervisory Board and the articles of association of TKH, both members may be re-appointed for a further period of two years and they have indicated that they are available for re-appointment. TKH will therefore nominate Mr. J.M. Kroon and Mrs. C.W. Gorter for re-appointment as members of the Supervisory Board for a term until the end of the AGM 2027.

Dividend proposal

The 2025 General Meeting of Shareholders will be asked to approve the payment of a 2024 cash dividend of €1.50 per (depositary receipt for a) share (2023: €1.70), amounting to a payout ratio of 60.5% of the net profit before amortization and one-off income and expenses attributable to shareholders (2023: 53.0%) and 60.0% of the net profit attributable to shareholders (2023: 41.7%). The dividend will be payable on May 23, 2025.

As of December 31, 2024, the total (depository receipt of) shares outstanding amounted to 42,198,429 of which 2,325,349 were treasury shares.

Strategy update: Focus and Optimization

With our Accelerate 2025 strategy we have created strong foundations with leading positions in markets such as tire building machines, machine vision for factory automation, integrated security systems and energy cable systems. We have expanded our production capacity in this area and have developed state-of-the-art technologies with distinctive USPs.

In the next strategic phase, we will focus on our activities which bring the best value creation potential, given our market leading positions and proprietary technologies on the back of the global trends

1) Focus on Automation and Electrification by leveraging our existing footprint and by deploying proprietary technologies

Within Automation, we will focus on production automation, inspection and security as core activities. In Electrification, we will build on our significantly expanded production capacity for offshore and onshore connectivity and capitalize on the substantial value creation opportunities. Our R&D competences, innovations, smart software, and AI will remain cornerstones to accelerate growth.

2) Further optimize our operations through integrations and divestments

Organizational optimization and integration will drive further cost efficiencies in our operations. We will continue to divest non-core business activities that are not related to Automation or Electrification. This includes our Digitalization activities within Smart Connectivity systems.

3) Capital allocation

The proceeds of the divestments will be used to further build on our core technologies in Automation and Electrification, while we aim to return excess cash to shareholders through dividends and/or share buybacks.

TKH plans to host a Capital Markets Day on September 25, 2025 to present an update on this strategy and the targets for the next phase.

Financial developments fourth quarter 2024

In the fourth quarter of 2024, turnover increased organically by 4.7% and EBITA excluding one-off income and expenses by 5.1% compared to Q4 2023. All segments contributed to the revenue growth, with Smart Vision systems’ revenue up 8.5% organically, Smart Manufacturing systems’ turnover increasing by 5.6% organically and Smart Connectivity systems up 1.0% organically. Smart Vision systems reported a record EBITA excluding one-off income and expenses, as both 2D and 3D Machine Vision and Security Vision benefitted, amongst others, from the delivery of larger orders secured earlier in the year. ROS reached 14.6% in the quarter.

Financial developments full year 2024

Turnover reached €1,712.7 million in 2024, a decrease of 7.3% (2023: €1,847.5 million), a large part of which was caused by divestments. Adjusted for acquisitions, divestments and currency effects, turnover decreased organically by 1.2%. Acquisitions accounted for +0.7% and divestments accounted for -6.8% of turnover. Of the three segments, Smart Manufacturing systems recorded turnover growth in 2024.

The geographical distribution of turnover shifted in favor of Asia and North America. The turnover share in the Netherlands declined slightly to 24% of total turnover (2023: 25%), while the share in Europe, excluding the Netherlands, declined to 35% (2023: 39%), partly caused by divestments. In Asia, the turnover share grew to 21% (2023: 19%), due to a larger share of tire building machines delivered to Asia, while turnover in North America grew to 15% (2023: 13%). The turnover share of the other geographical regions grew to 5% (2023: 4%).

The order intake in 2024 amounted to €1,911.4 million (2023: €1,834.8 million), resulting in an order book at year-end of €1,135.0 million (2023 €970.1 million). The order book at Smart Connectivity systems reached a record level of €493.6 million (2023: €214.8 million), driven by a number of large orders for inter-array cables. The order book at Smart Vision systems increased from €124.0 million at year-end 2023 to €139.9 million at year-end 2024. The order book at Smart Manufacturing systems decreased from €631.3 million at year-end 2023 to €501.5 at year-end 2024. The divestments of HE Systems and EKB Groep accounted for €40.0 million of the order decline in Smart Manufacturing systems.

The added value increased to 51.9% in 2024 (2023: 49.8%). All segments reported an increase in added value. Most notably Smart Connectivity systems’ added value went from 41.8% in 2023 to 44.0% in 2024. The increase in added value was mainly attributable to the elimination of EU anti-dumping duties on fibre optic cables, a change in product mix, and the impact of acquisitions and divestments.

Operating expenses (excluding one-off income and expenses, amortization and impairments) increased by 0.3% compared to last year. Acquisitions and divestments had a net impact of -3.1%. Operating expenses were impacted by the start-up and ramp-up of capacity related to strategic investments, as well as by payroll increases. Currency effects had a limited impact.

As a result, EBITA excluding one-off income and expenses decreased organically by 7.5% to €203.9 million in 2024, from €237.0 million in 2023. ROS decreased to 11.9% (2023: 12.8%). Inflationary effects, destocking at customers and start-up costs of our new factories all had a dampening effect on ROS. The ROS at Smart Manufacturing systems increased markedly to 19.1% (2023: 15.8%), driven by high-capacity utilization, implemented efficiency improvements, and the catch-up effects from the delivery of previously stored machines in the course of 2024.

In 2024, one-off expenses on EBITA-level amounted to €4.0 million (2023: one-off expenses of €2.0 million) mainly due to the €15 million cost-saving measures implemented in H2 2024. These included reorganization costs in Smart Vision systems for the integration in 2D Vision, restructuring costs in Smart Connectivity systems due to the centralization of fibre optic cable production in Poland, and acquisition and divestment costs.

Amortization increased to €60.8 million (2023: €56.9 million) due to the higher amortization of capitalized R&D, as a result of increased investments in previous years and higher amortization of purchase price allocations due to acquisitions. Impairments amounted to €8.5 million (2023: €3.7 million) for mainly underutilized right-of-use and fibre optics network related assets.

Net financial expenses increased to €29.3 million (2023: €22.1 million) due to the combination of higher debt levels and higher interest rates. The results from associates and subsidiaries amounted to €24.5 million (2023: € 51.5 million) and includes the one-off profits from the divestments of HE System Electronic and EKB Groep of €24.2 million (2023: divestment of CCG and TKH France of €54.8 million).

The normalized effective tax rate was stable at 24.4% in 2024 compared to 24.6% in 2023. TKH benefitted from R&D tax facilities in several countries.

Net profit before amortization of intangible non-current assets related to acquisitions and one-off income and expenses attributable to shareholders decreased by 24.2% to €98.9 million (2023: €130.5 million). Net profit decreased to €99.5 million (2023: €165.8 million). Earnings per share before amortization, one-off income and expenses amounted to €2.48 (2023: €3.21). Ordinary earnings per share were €2.50 (2023: €4.07).

Net bank debt according to bank covenants increased by €26.8 million from year-end 2023 to €496.0 million at year-end 2024. The main items affecting the debt level include the net investments in property, plant, and equipment of €98.7 million (€49 million of which is related to the strategic investment program), acquisitions (net €38.6 million), investments in intangible assets (€61.7 million), and dividends paid (€67.9 million). Divestments amounted to €60.3 million in 2024, including the €24.2 million one-off profit. At year-end 2024, €18.2 million assets were held for sale (year-end 2023: €18.0 million), related to the intended divestment of the test and measurement system activities, Dewetron. Cash flow from operating activities amounted to €196.2 million (2022: €152.9 million), an improvement due to a decrease in working capital in 2024 compared to an increase a year earlier. Working capital stood at 17.9% of turnover (2023: 16.7%). The net debt/EBITDA ratio, calculated according to TKH’s bank covenant, was 2.0, well within the financial ratio agreed with our banks. Solvency improved to 39.9% (2023: 39.3%).

At year-end 2024, TKH employed a total of 6,640 FTEs (2023: 6,899), 351 of which were temporary employees (2023: 434 FTEs).

Developments per technology segment

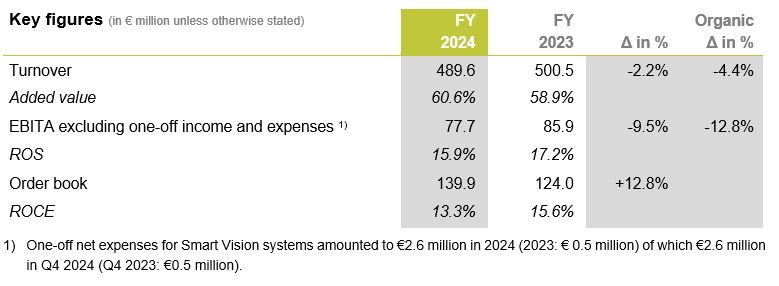

Smart Vision systems

In 2024, turnover in Smart Vision systems decreased by 2.2% to €489.6 million. Adjusted for acquisitions and currency effects, turnover decreased organically by 4.4%. The order book increased by 12.8% to €139.9 million (2023: €124.0 million) resulting from a strong order intake in Q4 2024. The added value increased from 58.9% to 60.6%. Due to higher operating expenses combined with lower turnover growth, EBITA excluding one-off income and expenses decreased 12.8% organically to €77.7 million and ROS reached 15.9%.

Vision Technology (85% of Smart Vision systems’ turnover) – In line with expectations, both Security Vision and Machine Vision posted a record Q4 2024 on the back of a strong order intake delivery and the delivery of some larger secured orders. In 2024, Security Vision’s turnover declined slightly, mainly due to the comparison with a strong 2023. In Machine Vision, 3D Vision recorded a decline in turnover due to weak market circumstances in solar and battery business. The return of the wood market and the contribution from Liberty Robotics, which was acquired in the second half of 2024, were not sufficient to offset this impact. 2D Vision recorded growth during the year as it benefitted from implemented customer excellence programs, and expansion into new end markets such as defense. In both 2D and 3D Machine Vision, further innovations accelerated by AI were brought to the market. Machine Vision also saw its share of customized solutions increase. During the year, steps were taken to consolidate the organization of TKH's 2D brands and to strengthen the supply chain, which, together with the implementation of cost-saving measures, resulted in one-off expenses of €2.6 million. These steps will benefit the results of 2D Vision from 2025 onwards. With the return of the wood market, new markets and solutions with Liberty Robotics, and a successful penetration into India, we expect the results for 3D Vision to have bottomed out in 2024 and to start growing. The growth in the order book is largely due to a number of larger security and parking automation projects in Security Vision and to some extent in 2D Machine Vision.

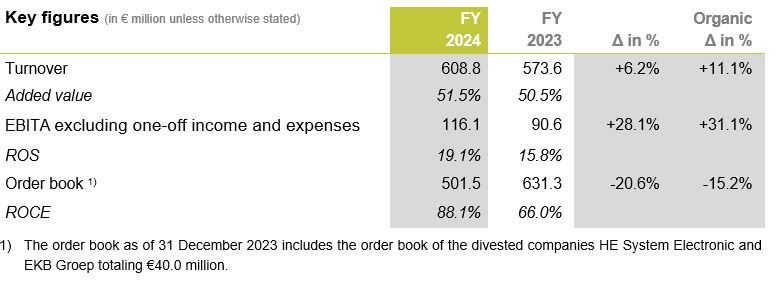

Smart Manufacturing systems

Smart Manufacturing systems turnover grew strongly during the year, although growth slowed down in the second half of 2024, in line with expectations, partly explained by the strong H2 2023. Adjusted for currency effects and divestments, turnover in 2024 grew organically by 11.1%. During 2024, HE System Electronic (2023 turnover €20.7 million) and EKB Groep (2023 turnover €35.5 million) were divested. The order book at €501.5 million decreased by 20.6% (15.2% decrease organically) compared to its record level of € 631.3 million on December 31, 2023. The added value increased further to 51.5% (from 50.5% previously), due to a combination of product mix and price increases being passed on to customers. EBITA excluding one-off income and expenses was up 31.1% organically at €116.1 million, as the implemented efficiency improvements continued to pay off, in combination with the high-capacity utilization at Tire Building systems. As a result, the ROS expanded to 19.1% (2023: 15.8%), with ROS reaching 20.3% in Q4 2024.

Tire Building systems (83% of Smart Manufacturing systems’ turnover) – Tire Building systems benefitted from a very strong year in 2024, driven by a record order book and the catch-up effect of deliveries, following the easing of earlier supply chain constraints. Together with the efficiency improvements implemented during the year, this led to a strong operational performance. The production facilities in Poland were further expanded in the first half of 2024. The order for a UNIXX system booked at the beginning of 2024 is scheduled for delivery and installation in the second half of 2025, with further strong market interest. The revolutionary UNIXX technology, implemented in newly released tire component production machines such as UNIXX Beltmaker and Revolute, as well as in tire building machines, continues to gain traction. During the year, AI-powered features were introduced, including Foreign Object Detection, which is based on our proprietary high-speed algorithm that analyzes images in real time with unprecedented accuracy, while minimizing the number of false positives. The lower order intake in 2024, both for passenger and truck tire machines was mainly related to a decline in demand at Tier 1 customers, whereas order intake from Tier 2 and 3 customers remained at similarly high levels compared to previous years. The drivers for tire building systems remain very strong, as the need for more flexibility in production, increased sustainability demands, and the need for higher levels of automation will fuel future demand for more advanced tire building production.

Other – During the year, the divestments of HE System Electronic and EKB Groep were closed and Dewetron was reclassified to “Held for sale.” New orders were received for the Indivion, strengthening our position in the Nordics region.

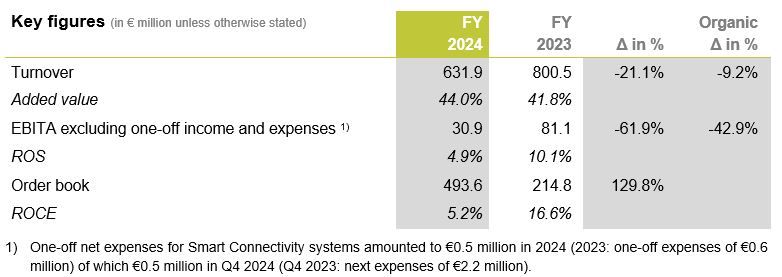

Smart Connectivity systems

Turnover in Smart Connectivity systems decreased 21.1% to €631.9 million in 2024 (2023: €800.5 million). Adjusted for the divestment of the commodity connectivity activities in France in September 2023 and currency effects, turnover declined organically by 9.2%. The order book grew strongly to €493.6 million (2023: €214.8 million), with the 129.8% increase coming mainly from inter-array cable orders, including the €200 million turnkey inter-array cable project with Inch Cape, which includes the survey, engineering, manufacturing, testing, supply and installation of the inter-array cables. Added value as a percentage of turnover increased to 44.0% from 41.8% in 2023, mainly due to a shift in product mix, elimination of anti-dumping duties on fibre cables and the divestment. EBITA excluding one-off income and expenses decreased organically by 42.9% to €30.9 million, impacted by lower volumes, start-up and ramp up costs of the new Eemshaven factory, and low levels of utilization in inter-array and fibre optic cables. ROS decreased to 4.9%.

Electrification (48% of Smart Connectivity systems turnover) –TKH has invested significantly in additional capacity in offshore wind inter-array cables, and high and medium voltage onshore energy cables in anticipation of substantial market growth in the coming years. The €150 million strategic investment into Electrification is now completed, and the ramp-up of serial production at the new Eemshaven plant for inter-array offshore wind cables, which was initially postponed, is expected to commence shortly . In the past months, the issues in what is considered the most critical production processes have been solved. The remaining production stages are less complex and have already been successfully completed for shorter lengths. To meet the demand for inter-array cables, it was decided to continue the production of inter-array wind cables at the Lochem plant. The demand for onshore energy cables in the Netherlands remained weak due to destocking by utility companies. We made good progress in positioning our high- and medium-voltage cables outside the Netherlands in Europe. Our sales funnel for inter-array cables remains high with more than >10,000 km up until 2030. In anticipation of the planned growth and driven by the large order intake, we expanded our staff. The aforementioned limitations to our turnover growth in inter-array, high- and medium-voltage cables, combined with higher start-up and ramp-up costs impacted the EBITA excluding one-off income and expenses in 2024.

Digitalization (29% of Smart Connectivity systems turnover) – Digitalization continued to be impacted by a deteriorating market for fibre optic cables in Europe, due to low levels of investment in the rollout of European fibre networks, a strong destocking effect, as well as pricing pressure due to high inventory levels in the Chinese market. The elimination of EU anti-dumping duties could not compensate for the low utilization rate and ramp-up costs of our new factory in Poland. In 2024 we decided to close the fibre optic cable production in the Netherlands and consolidate production in Poland, which will reduce our operating expenses from Q2 2025 onwards.

Other (23% of Smart Connectivity systems turnover) – TKH’s specialized and customized connectivity systems for the machine-building and robotics industries continued to be impacted by the weak German economy.

Outlook

TKH has made strong progress in its strategic positioning with the completion of the €200 million strategic investment program, which will start to pay off in 2025. This, combined with the strong order book, will position us well for 2025.

The first quarter of 2025 will be weak due to seasonality, the ramp-up of the Eemshaven plant, and continued weakness in the fibre optic cable market. For the full year, we expect turnover and EBITA excluding one-off income and expenses growth to return in Smart Vision systems, driven by the stronger order book, expected market share growth in new markets, and the implemented cost-saving measures. In Smart Manufacturing systems, turnover and EBITA excluding one-off income and expenses are expected to decrease organically due to the lower order intake in 2024 and the comparison with a very strong 2024, which benefitted from catch-up effects. In Smart Connectivity systems, we expect the new production capacity and the high order intake in 2024 to contribute to significant turnover and EBITA excluding one-off income and expenses growth in Smart Connectivity systems.

Barring unforeseen circumstances, on balance we anticipate organic growth in turnover and EBITA excluding one-off income and expenses in 2025.

TKH will provide a more specific outlook for the full year of 2025 at the presentation of its interim results in August 2025.

You can follow the presentation of the full-year results on March 4, 2025 at 10:00 CET via video webcast (www.tkhgroup.com).

Haaksbergen, March 4, 2025