Full year 2015 Results

Press Release

Haaksbergen, the Netherlands

8 Mar 2016

Increase in result supported by good performance Building Solutions

Highlights Q4

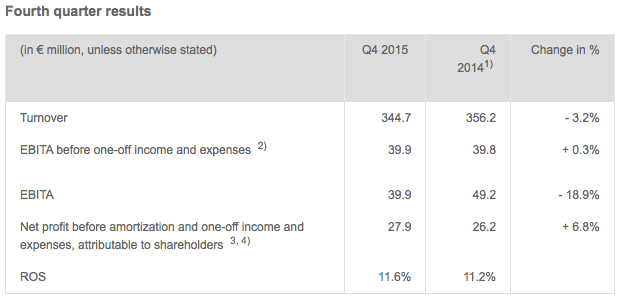

- Turnover down 3.2% to € 344.7 million, organic turnover decline of 6.6%.

- Turnover Building Solutions increases with 11.2%, of which 1.9% organic.

- Turnover decline of 14.1% at Industrial Solutions, in line with the reduced order intake in the previous quarters – turnover Telecom Solutions declines 3.8%.

- EBITA before one-off income and expenses increases 0.3% despite extremely strong Q4 2014; sharp increase EBITA Building Solutions, partly by good contribution from acquisitions.

- ROS rises to 11.6% due to focus on more profitable turnover and cut-back in turnover with low added value.

- Increase of 6.8% in net profit before amortization and one-off income and expenses.

Highlights 2015

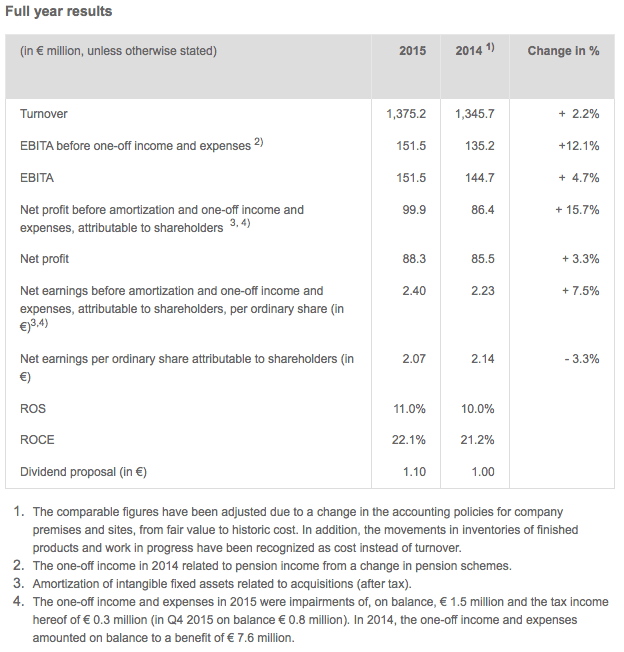

- Turnover up 2.2% at € 1,375.2 million, organic turnover decline of 2.6%.

- EBITA before one-off income and expenses up 12.1% because of acquisitions and focus on vertical growth markets.

- Increase of 15.7% in net profit before amortization and one-off income and expenses.

- Targets ROS and ROCE achieved.

- Increase medium-term ROS target to 11-12% and ROCE to 20-22%.

- Dividend proposal of € 1.10 per (depository receipt for an) ordinary share.

Alexander van der Lof, CEO of technology company TKH:

“We were able to close the year 2015 with a positive result, despite the negative impact of the low order intake from China since Q4 2014 in the sub segment manufacturing systems. The substantial increase in the result of Building Solutions created more balance in TKH’s overall result. Herewith we have succeeded in giving substance to our goal to reduce the cyclicity of the total result. The benefits of the investments we have made in recent years to structurally improve the result of Building Solutions, have clearly borne fruit. This success is largely the result of good acquisitions, focus on the vertical growth markets and R&D investments. The solid progress we have made in the strategic development of TKH enabled us to realize our ROS target within a year and we have therefore decided to once again raise the medium-term bandwidth for our ROS target to 11-12%. It is extremely important that we keep the right balance in the realization of the margin on the one hand and the necessary investments in R&D to safeguard TKH’s continuity and the development of value creation in the long term, on the other hand.”

Financial developments

In 2015, turnover increased € 29.5 million (2.2%) to € 1,375.2 million (2014: € 1,345.7 million). Acquisitions contributed 3.1% to turnover. Lower raw materials prices had a negative impact of 0.2% on turnover (2014: 0.7%), while stronger foreign currencies compared with the euro had a positive impact of 1.9% on turnover. On balance, organic turnover declined by 2.6%. This was partly due to the deliberate cut-back of less profitable turnover, in line with TKH’s strategic focus.

Building Solutions booked strong turnover growth of 16.9%. Turnover at Telecom Solutions declined slightly, by 0.8%, while Industrial Solutions recorded a decline of 7.8%. For the full year 2015, Industrial Solutions’ contribution to turnover dropped to 46% from 51%, while the contribution from Building Solutions increased to 42%, from 37%. The contribution from Telecom Solutions remained stable at 12%. Innovations once again made a sizeable contribution to turnover, accounting for 23.5% of turnover in 2015 (2014: 22.8%).

The gross margin was up at 46.0% in 2015, from 42.8% in 2014, thanks to the acquisition of the Commend-group and an improved product mix. The operating costs (excluding one-off pension income in 2014) as a percentage of turnover rose to 34.9%, from 32.7% in 2014. That increase was largely due to higher in-house production and therefore reduced outsourcing to third parties, plus an increase in R&D costs. Spending on R&D rose to € 46.5 million in 2015 (2014: € 41.9 million). Depreciations came in at € 21.4 million, this was € 1.6 million higher than in 2014, due to the higher level of investments in recent years.

The operating result before amortization of intangible assets and one-off income and expenses (EBITA) increased 12.1% at € 151.5 million in 2015, from € 135.2 million in 2014. At Building Solutions, EBITA was up 49.9% due to the acquisition of the Commend-group, a rise in turnover in vision & security systems and connectivity systems, together with a related improvement in efficiency and utilization rates at TKH’s production plants. EBITA at Telecom Solutions was up 8.8%, while EBITA at Industrial Solutions declined by 7.4% compared to 2014. ROS rose to 11.0% in 2015 (2014: 10.0%) and was therefore at the higher end of the medium-term ROS target TKH had communicated (bandwidth of 10-11%) previously.

Amortization costs increased by € 5.4 million to € 31.6 million due to the acquisition of the Commend-group and higher investments, especially in R&D. In addition, we recognized an impairment of € 1.8 million from depreciations on capitalized R&D projects and a release of financial obligations for earn-out and put-options of € 0.3 million, which on balance resulted in a one-off charge of € 1.5 million.

In 2015, financial expenses declined € 1.2 million to € 8.2 million. This improvement was due to lower interest rates and reduced credit spreads, as well as interest swaps that matured in 2014. Currency exchange effects had a positive impact of € 0.4 million, compared to a negative impact of € 0.9 million in 2014. The result from participations improved by € 0.5 million.

The tax rate remained stable at 20.6% of the pre-tax profit. The application of the Dutch innovation box facility similar to last years had a positive impact on the tax rate.

Net profit before amortization and one-off income and expenses attributable to shareholders was up 15.7% at € 99.9 million in 2015 (2014: € 86.4 million). Net profit for 2015 increased to € 88.3 million (2014: € 85.5 million). In 2014, TKH’s results included one-off net pension income of € 9.4 million. Earnings per share before amortization and one-off income and expenses came in at € 2.40 (2014: € 2.23). Ordinary earnings per share were € 2.07 (2014: € 2.14).

The cash flow from operating activities rose to € 181.6 million in 2015 (2014: € 94.9 million) thanks to a substantial reduction in working capital whereas 2014 showed an increase. At year-end 2015, working capital as a percentage of turnover decreased 11.4% (2014: 13.8%). Net investments in tangible fixed assets in 2015 stood at € 37.2 million (2014: € 33.7 million). A considerable part of this was related to investments in the production plants, including the expansion of capacity for the sub-segments building connectivity systems, manufacturing systems, vision & security systems and fibre network systems. In addition, TKH invested € 25.4 million in intangible fixed assets, primarily R&D, patents, licenses and software (2014: € 22.5 million). Expenditure related to acquisitions was € 49.7 million and was primarily related to the acquisition of the Commend-group. In addition to this acquisition, TKH acquired a 49% participation in Commend Australia and the outstanding minority third-party shareholding in Commend Benelux and Schneider Intercom. In addition, in 2015 TKH acquired the remaining minority interest in Augusta Technologie AG in a squeeze-out procedure. The acquisition of the minority third-party shareholding resulted in expenses of € 25.2 million in 2015.

Net bank debt, calculated in accordance with the bank covenants, declined by € 3.8 million year-on-year to € 161.0 million at year-end 2015. The solvency ratio increased slightly to 42.2% (2014: 41.9%). Herewith TKH operates well within the financial ratios agreed with the banks. The net debt/EBITDA ratio stood at 0.9 and the interest coverage ratio at 22.5.

At year-end 2015, TKH had a total workforce (FTEs) of 5,387 and employed a further 441 (FTE) temporary employees. The increase in employee numbers was largely due to the acquisition of the Commend-group and the further bolstering of the organization in the field of R&D and commerce in Building Solutions.

Progress realization targets and execution strategy

TKH once again devoted considerable attention to its strategic development in the year under review. The focus on our core technologies and the seven vertical growth markets helps us to pursue ambitious growth targets. The turnover targets in our vertical growth markets have resulted in a well-organized implementation of a several growth plans, which has resulted in an acceleration in the realization of our ROS and ROCE targets. On that basis and on the basis of the potential we see in our seven growth markets, we have again decided to adjust our targets upwards. For the medium term, we have adjusted the ROS target to a bandwidth of 11-12% (from 10-11%) and the ROCE target to a bandwidth of 20-22% (from 18-20%).

The perspective for the growth scenarios per vertical growth market on the medium-term continued to improve. The overall growth in the vertical growth markets in 2015, excluding the tire building industry, was € 60 million. In the tire building industry our turnover was negatively influenced due to a reluctance to investments in China, where we realized more than 60% of order intake in 2014, compared to less than 10% in the year under review. However, the targeted turnover growth in the tire building industry for the coming years is on track thanks to amongst others the positive development of our position with the five major tire manufacturers.

The share of the vertical growth markets in TKH’s total turnover has meanwhile increased to € 697 million (50.7%). In light of the fact that the average margin in these vertical growth markets is higher than the TKH average, this will be an important driver for the development of ROS within TKH. Based on the technology roadmaps and the proposed roll-out of the related new business, we expect organic turnover growth in this area to be somewhat limited in the vertical growth markets in the next two years, however, growth will materialize from 2018. Based on the defined growth plans and progress we have made, we expect turnover in our seven vertical growth markets to increase by € 300 million to € 500 million in the next 3‑5 years.

Innovations accounted for 23.5% of TKH’s turnover in 2015, which is again at a very high level and once again exceeded our target of 15% of turnover from innovations introduced in the market over the past two years. These innovations helped TKH to increase its market share in 2015.

Developments per solutions segment

Telecom Solutions

Telecom Solutions develops, produces and supplies systems ranging from basic outdoor infrastructure for telecom and CATV networks through to indoor home networking applications. The focus of the business is on the delivery of completely worry-free systems for its clients, thanks to the system guarantees it provides. Around 40% of the portfolio consists of hub-to-hub optical fibre and copper cable systems. The remaining 60%, consisting of components and systems in the field of connectivity and peripherals, is deployed primarily in network hubs.

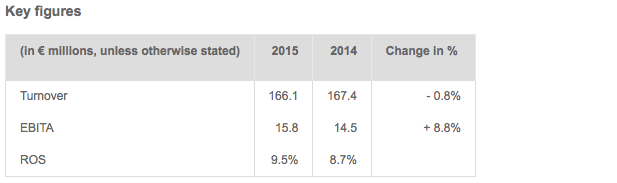

Turnover within the Telecom Solutions segment declined by 0.8% to € 166.1 million. Turnover fell by 2.4% organically, while currency exchange rates had a positive impact of 1.6% on turnover. The organic decline was due to the sub segment fibre network systems, which lagged in the strong second and fourth quarter of 2014. The demand for optical fibre declined in the Netherlands and the increase in turnover in Poland, Germany and China was not enough to completely offset this decline.

EBITA rose by € 1.3 million. The ROS improved to 9.5% from 8.7% because of efficiency improvements in production, cost savings and an improved margin in the international roll-out. The increase in margin was also boosted by strong demand in China.

Indoor telecom & copper networks - home networking-systems, broadband connectivity, IPTV software solutions, copper cable, connectivity systems and components, active peripherals – turnover share 5.3%

Turnover in this sub segment increased 0.5%. In the first half of the year, turnover increased in home networking systems, largely due to higher consumer spending in the Benelux. In the second half of the year, turnover was down as a result of a further increase in investments in passive components for copper networks and a continued shift in the priority to invest in optical fibre networks.

Fibre network systems - optical fibre, optical fibre cables, connectivity systems and components, active peripherals – turnover share 6.8%

Turnover in this sub segment declined by 1.7%. Turnover in the second half increased compared to the first half, as well as compared to the second half last year. In the Netherlands and Scandinavia, investments in optical fibre networks fell considerably due to the fact that telecom operators have temporarily called a halt to the roll-out of optical fibre networks for FTTH (Fibre to the Home) and are currently focusing on utilizing the capacity of existing optical fibre and copper networks. However, investments in optical fibre networks in Eastern Europe, Germany and China increased and this largely offset the decline in demand in the Netherlands and Scandinavia. The additional production capacity in China that was taken into operation at the end of the first quarter of 2015 also had a positive impact on efficiency and margins. The scarcity of optical fibre on the Chinese market also had a positive impact on margins, thanks to which, on balance, the result continued to improve. In France we won a very good contract for the robotized connection of cables (SAODF- Semi-Automatic Optical Distribution Frame) in the network hubs.

Building Solutions

Building Solutions develops, produces and delivers solutions in the field of efficient electro-technical technology, ranging from applications within buildings to technical systems which, linked to software, provide efficiency solutions for the care and security sectors. TKH’s know-how in this segment is focused on vision technology and connectivity systems combined with efficiency solutions to reduce the throughput-time for the realization of installations within buildings and industrial automation. In addition, TKH’s focus in this segment is on intelligent video, intercom and access monitoring systems for a number of specific sectors, including elderly care, parking, marine, oil & gas, tunnels and security for buildings and work sites.

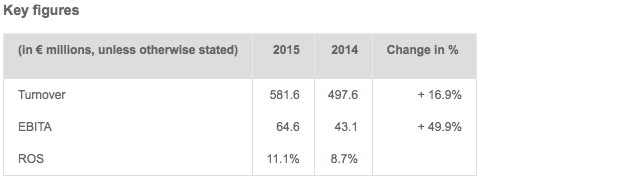

Turnover in the Building Solutions segment increased 16.9% at € 581.6 million. Acquisitions accounted for growth of 8.5% while exchange rate effects had a positive impact of 3.3% on turnover. Lower raw materials prices had a negative impact of 0.5% on turnover. Organic growth came in at 5.6% on balance. This growth was largely realized in the vertical growth markets vision, parking and marine, oil and gas industry. We also noted the first signs of recovery in the European building and construction sector.

EBITA came in 49.9% higher at € 64.6 million, partly due to the acquisition of the Commend-group and turnover growth in both sub segments. ROS rose to 11.1% in 2015, from 8.7% in 2014.

Vision & Security systems – vision technology, systems for CCTV, video/audio analysis and detection, intercom, access control and registration, central control room integration, care systems – turnover share 25.7%

Turnover in the sub segment was 25.1% higher, with a sizeable contribution from the acquisition of the Commend-group (+14.9%). Currency exchange rate effects boosted turnover by 3.4%. Organic growth was 6.8%. The vertical growth markets made a positive contribution to turnover growth. Thanks to the high gross margin in this sub segment, turnover growth led to an even higher increase in result. The innovations and distinctive technologies in this sub segment are an excellent response to the need among our customers to work more securely and efficiently. The share of turnover generated outside the Netherlands increased sharply, thanks to the large number of international projects, especially in North America. There was also less reluctance to invest in the building and construction sector and we saw an increase in the number of new-build homes in the Benelux. However, there was a drop in the number of large projects in the utilities sector and in the field of infrastructure. TKH increased its R&D spending to increase the competitive edge our technology gives us in this market.

Connectivity systems – specialty cable (systems) for shipping, rail, infrastructure, wind energy, as well as installation and energy cable for niche markets – turnover share 16.6%

Turnover in this sub segment increased 6.1%, with 3.1% of this due to currency effects, while lower raw materials prices had a negative impact of 1.1%. Organic turnover was up 4.0%, with organic growth higher in the second half than in the first half. Here too, the vertical growth markets had a positive impact and we were able to realize growth despite stagnant market volume in the building and construction sector. Especially the results in the vertical growth markets marine, oil and gas contributed particularly well. The turnover growth was realized at lower cost levels, thanks to a strong focus on efficiency improvements, which resulted in improved EBITA.

Industrial Solutions

Industrial Solutions develops, produces and delivers solutions ranging from specialty cable, plug and play cable systems to integrated systems for the production of car and truck tires. The company’s know-how in the automation of production processes and improvements in the reliability of production systems gives TKH the differentiating potential to respond to the increasing desire to outsource the construction of production systems or modules in a number of specialized industrial sectors, such as tire manufacturing, robotics, medical and machine building industries.

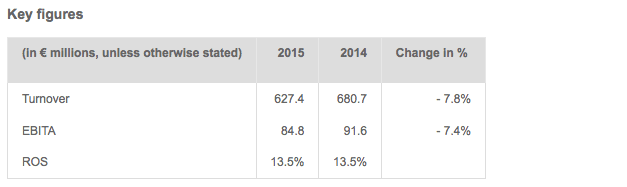

Turnover in the Industrial Solutions segment declined by 7.8% to € 627.4 million. Currency effects had a positive impact of 1.0% on turnover. The on average lower raw materials prices had a negative impact on turnover of 0.3%. Organic turnover declined by 8.5%. The reluctance to invest in China, which was particularly notable in the robot and machine industry, including tire building systems, resulted in a decline in both order intake and turnover in 2015.

EBITA declined by 7.4% to € 84.8 million. Thanks to effective cost controls, improved efficiency and increased in house production, ROS remained stable at 13.5% (2014: 13.5%).

Connectivity systems – specialty cable systems and modules for the medical, robot, automotive and machine building industries – turnover share 17.2%

Turnover in this sub segment was down 1.6%, partly due to the 0.6% negative impact on turnover from charged-on lower raw materials prices and currency effects. We saw a slight improvement in the second half of the year in terms of organic growth. Turnover developed positively in the medical industry. Order intake from the German robotics and machine industry saw a particularly strong decline, also as a result of the reluctance to invest in China. As a result of customers reduced their inventories in the fourth quarter, which had a negative impact on turnover for the connectivity segment. The margin improved slightly due to a greater proportion of innovative cable solutions for medical equipment. The higher proportion of cable systems also contributed to the improved margin. We expect the share of turnover from complete systems to continue to increase in the coming years.

Manufacturing systems – advanced manufacturing systems for the production of car and truck tires, can washers, test equipment, product handling systems for the medical industry, machine operating systems – turnover share 28.4%

Turnover fell by 11.2% in this sub segment. This decline was in line with the reduced order intake in the manufacturing systems segment in the preceding quarters due to reluctance to invest in the tire manufacturing industry in China. The drop in turnover in the second half of the year came in at 16.6% and was thus clearly higher than the 5.4% drop in the first half of the year. The order intake in manufacturing systems for the tire building systems component was € 60 million in the fourth quarter and € 285 million for the full year 2015. However, a considerable proportion of systems ordered by customers in China in 2014 were delivered in 2015, which led to a considerable improvement in working capital. The order intake outside China was broad-based, both in terms of customers and in terms of geographic spread. We are on track to realize turnover growth in the tire building industry for the coming years because of the development of our position with the five major tire manufacturers. In addition, our position in the truck tire market will be strengthened by our new generation systems for truck tire manufacture, under the name MILEXX. In the third quarter of 2015, we decided to increase the capacity for the production of tire building systems in Poland.

The decline in turnover in tire building systems was partly offset by some large-scale projects in measuring and control systems for the automotive and aerospace industries and elsewhere. We also successfully launched a new generation of medicine distribution systems and we will continue with the roll-out of these systems in 2016.

Reappointment Supervisory Board

At the General Meeting of Shareholders on 26 April 2016, Mr. R. L. van Iperen will step down as member of the Supervisory Board in line with the prevailing rotation schedule. Mr. Van Iperen is eligible for reappointment for a next term and he will be nominated for reappointment during the General Meeting of Shareholders on 26 April 2016.

Dividend proposal

At the Annual General Meeting to be held on 26 April 2016, TKH will propose the payment of a dividend of € 1.10 per (depositary receipt for a) share (2014: € 1.00). Based on the number of outstanding shares at year-end 2015, this amounts to a pay-out ratio of 45.9% of the net profit before amortization and one-off income and expenses, and 52.0% of the net profit. TKH will propose the payment of an optional dividend in cash or in shares, which will be charged to the reserves.

TKH will determine the dividend payment in shares one day after the end of the optional period on the basis of the average price of TKH shares during the last five trading days of the optional period, which shall end on 17 May 2016. The dividend will be payable, in cash or in shares, on 20 May 2016.

Outlook

Global economic conditions are mixed. The impact of and uncertainty regarding the economic developments in China has now led to uncertainty about global economic developments in the year ahead, which has in turn resulted in reluctance to invest in the industrial sector.

We see challenges and opportunities per Solutions segment. Our core technologies put us in a solid position to realize continued growth. This gives us good grounds to expect that we will be able to increase turnover by € 300 million to € 500 million in the seven selected vertical growth markets in the next 3-5 years.

Barring unforeseen circumstances, we expect the following developments in 2016:

Telecom Solutions

Investments in Europe and China in optical fibre networks are expected to increase. Due to our investments in market penetration in recent years, growth potential for TKH will be largely focused in Europe. The investments we made in 2015 to expand our production capacity and the proposed additional investments in 2016 will help us to take advantage of growth opportunities and increase efficiency in our plants.

Building Solutions

In the sub segment vision & security systems, there is a positive outlook for growth in investments, which will result in a further increase in demand for these systems. The trend towards continuous renewal of inspection applications, together with the desire to realize increasingly accurate tolerances, is a positive development for TKH in terms of its ability to position its cutting-edge vision technologies and further expand its market share. The connectivity segment will feel the impact of reluctance to invest within the marine, oil and gas industry. On the other hand, there are signs of growth in investments in the building and construction sector and the energy/infra sector.

Industrial Solutions

In China, there is still a strong reluctance to invest in capital goods. We expect this reluctance to persist for the coming year. The lower order intake, which has been down since the beginning of 2015, has an impact on the results for the first half 2016. However, the outlook for an increase in order intake in 2016 compared to 2015 is positive, despite the reluctance in China. We expect the capacity expansions we have realized to be particularly opportune in the second half of 2016, enabling to respond effectively to meet demand. In anticipation of the expected higher order intake, cost levels will be higher than usual in the first half of the year and will support the medium-term growth potential to enable us to increase our turnover in this segment.

As usual, TKH will give a specific forecast for the full-year profit for 2016 at the presentation of its interim results in August 2016.

The complete press release can be downloaded in PDF