Full year 2013 Results

Press Release

Haaksbergen, the Netherlands

12 Mar 2014

Profit growth driven by focus on core technologies and vertical growth markets

Highlights Q4

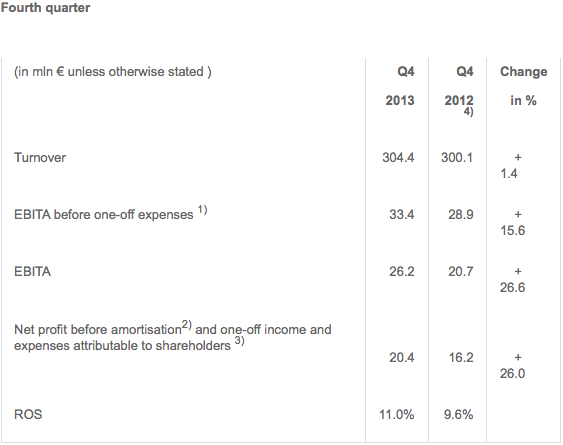

- Organic turnover growth of 1.9%.

- EBITA before one-off expenses 15.6% higher thanks to sharp results improvement at Building Solutions and Industrial Solutions.

- Increase of ROS to 11.0%

- One-off charge of € 7.2 million related to additional efficiency improvement programme at Building Solutions.

Highlights 2013

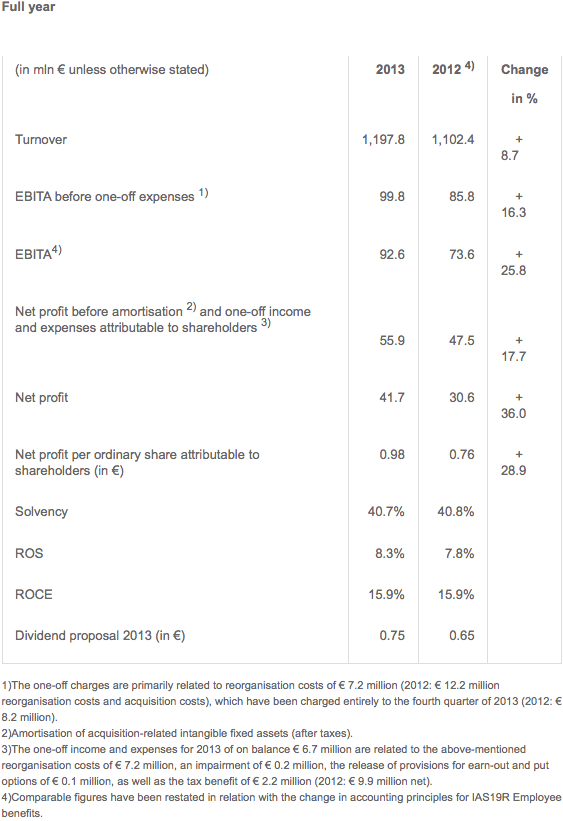

- Turnover up 8.7% at € 1.2 billion, organic growth 4.2%

- EBITA before one-off expenses 16.3% higher at € 99.8 million.

- Net profit before amortisation and one-off income and expenses up by 17.7%.

- Record order intake at Industrial Solutions – further breakthrough in positioning in tyre-manufacturing industry.

- Focus on vertical growth markets contributes to increase in ROS.

Dividend proposal € 0.75 per (depositary receipt for an) ordinary share.

Alexander van der Lof, CEO of technology company TKH:

“Despite the economic headwinds, TKH booked strong growth in both turnover and profit. So we are confident that TKH is in a good position for the year ahead. Certainly given that the economy currently looks to be on the road to recovery and given that in recent quarters order intake improved in most of the segments in which TKH is active. The profit improvement over the course of the year was also thanks to our focus on the seven high-growth vertical markets we have identified and on which we have focused our efforts for the past 12 months. This has enabled us to take full advantage of the opportunities in these markets. Combining our strengths in the high-growth vertical markets has also deepened the synergies between the technologies and the companies in the group. Thanks to this, TKH is even stronger and fitter.”

Financial developments

Turnover came in € 95.5 million higher (8.7%) at € 1,197.8 million in 2013 (2012: € 1,102.4 million). Acquisitions accounted for 5.7% of turnover. Lower raw materials prices had a negative impact of 1.2% on turnover. On balance, organic turnover growth came in at 4.2%.

Building Solutions booked the strongest turnover growth, with 12.2% higher turnover. Turnover at Industrial Solutions was up 10.7%. Telecom Solutions on the other hand saw turnover drop by 6.2%. In the full year 2013, the share of turnover accounted for by Industrial Solutions increased to 46% from 45%, while the share of Building Solutions rose to 41% from 40%. The share accounted for by Telecom Solutions fell to 13% from 15%. Innovations once again made a strong contribution to turnover, accounting for 21.2% of turnover in 2013 (2012: 21.2%).

The gross margin rose slightly to 41.7% in 2013 from 40.9% in 2012, due to acquisitions. Operating costs, excluding one-off charges and acquisitions, as a percentage of turnover fell to 32.6% in 2013, from 33.1% in 2012, thanks to the efficiency improvement measures taken in 2012. Depreciation came in € 2.0 million higher than in 2012 (€ 17.5 million), largely due to the acquisition of Augusta and higher investment levels in 2012 and 2013.

TKH’s operating result before amortisation of intangible assets and one-off income and expenses (EBITA) came in 16.3% higher at € 99.8 million in 2013, compared with € 85.8 million in 2012. At Building Solutions, EBITA came in 74.4% higher, with just over half of this growth due to acquisitions. At Industrial Solutions, EBITA fell by 2.4% due to a weak first half year. In the second half of the year, Industrial Solutions booked a 23.6% increase in EBITA. At Telecom Solutions, EBITA was 4.3% lower than in 2012. ROS for the TKH group as a whole rose to 8.3%, from 7.8% in 2012.

In the fourth quarter of 2013, TKH launched an additional efficiency improvement programme, largely related to the deterioration of the market conditions in the building and construction industry and TKH’s desire to book continued improvement in the return on sales in the Building Solutions segment. TKH took a one-off charge of € 7.2 million for this efficiency improvement programme. TKH expects these measures to result in annual savings of approximately € 5 million from 2014 onwards.

EBITA including this one-off charge came in € 19.0 million higher (25.8%) at € 92.6 million.

Amortisation charges increased by € 4.2 million to € 25.1 million (2012: € 20.9 million) due to the acquisition of Aasset Security, Augusta Technologie and Park Assist. TKH also took an impairment charge of € 0.2 million.

Financial income and expenses rose to € 15.2 million in 2013, from € 12.1 million in 2012. This increase was largely the result of higher amortisation of capitalised financing costs. These included a one-off charge of € 1.6 million, due to refinancing. In addition, currency exchange had a negative impact of € 0.6 million compared with 2012. As a result of the change in IFRS related to pension schemes, the interest component is now reported under financial expenses, which had a negative impact of € 0.4 million. Interest expenses dropped slightly by € 0.2 million to € 11.2 million.

The result from participations came in at € 1.4 million in 2013, thanks largely to positive results from the Chinese participation Shin-Etsu (Jiangsu) Optical Preform and dividends received.

TKH recorded extraordinary income of € 0.1 million, due to the release of the provision for earn-out and put options held by minority shareholders.

The tax rate fell to 22.5% in 2013, from 23.9% in 2012. As in 2012, the application of the Dutch innovation box facility had a positive impact on the tax rate.

Net profit before amortisation and one-off income and expenses attributable to shareholders came in at € 55.9 million in 2013 (2012: € 47.5 million), a rise of 17.7%. Net profit for 2013 rose to € 41.7 million (2012: € 30.6 million). Earnings per share before amortisation and one-off income and expenses amounted to € 1.48 (2012: € 1.27). The ordinary earnings per share came in at € 0.98 in 2013 (2012: € 0.76).

Operational cash flow rose to € 78.6 million in 2013 (2012: € 75.2 million). In 2013, working capital as a percentage of turnover came in at 13.2%, virtually unchanged from the 13.1% recorded in the previous year. Net investments in property and equipment came in at € 18.7 million in 2013 (2012: € 25.7 million). A large portion of this was related to investments in TKH’s production facilities. In addition, TKH invested a net € 15.5 million in acquisitions and participations and € 16.8 million in intangible fixed assets, largely accounted for by R&D, patents and licences (2012: € 14.1 million). TKH’s net bank debt decreased € 2.6 million to € 185.6 million by year-end 2013, compared with year-end 2012. Solvency fell to 40.7% (2012: 40.8%). TKH is operating well within the financial ratios agreed with its banks. The net debt/EBITDA ratio stood at 1.5 and the interest coverage ratio at 10.9.

TKH had a total workforce of 4,802 (FTEs) at year-end 2013 (2012: 4,736). The increase in the number of employees was largely due to the sharp increase in activities at Industrial Solutions.

Progress in realisation of targets and strategy

TKH’s strategy, launched in late 2012, of focussing on four core technologies - connectivity, vision, communications and manufacturing systems – in combination with seven vertical high growth markets – optical fibre networks, parking, tunnels, care, marine - oil & gas, industrial machine vision and tyre manufacture – has added a new dimension to TKH’s market positioning and potential. TKH sees a growth perspective of € 300 million to € 500 million in turnover in three to five years for these seven vertical growth markets. This was based on the normalised 2012 turnover of € 450 million for these seven vertical markets, including the full effect of acquisitions in 2012. In 2013, TKH increased turnover by € 50 million in these markets.

By choosing to focus on these high-growth vertical markets, TKH has put itself in a good position to improve ROS and ROCE. TKH also sees growth potential in the other markets segments, partly thanks to efficiency measures we have taken and partly thanks to growth we can realise on the back of improved market conditions or TKH’s improved market position, which creates scale-related efficiencies.

The ROS before one-off income and expenses rose to 8.3% in 2013, from 7.8% in 2012. After a weak first quarter, the remainder of the year showed a steady increase, as ROS increased to 11.0% in the fourth quarter, from 9.6% in the same period of 2012. It should be noted, however, that the fourth quarter is traditionally the best performing in terms of seasonal patterns. The above means TKH once again moved closer to its target of a ROS bandwidth of 9-10% over the full year.

The increase in ROS had a positive impact on the ROCE, partly thanks to the fact that the growth in results was largely due to organic growth, combined with a limited increase in invested capital. The acquisition of the majority stake in Augusta in 2012 led to a drop in ROCE in 2012. Due to investments and the capitalisation of the technology base we have created in recent years, ROCE was 15.9% in 2013 (2012: 15.9%).

The innovation component in TKH’s turnover remained high at 21.2% and was once again well above TKH’s target of generating 15% of its turnover from innovations launched on the market over the past two years.

Developments per solutions segment

Telecom Solutions

Profile

Telecom Solutions develops, produces and supplies systems ranging from basic outdoor infrastructure for telecom and CATV networks through to indoor home networking applications. The focus of the business is on the delivery of completely worry-free systems for its clients, thanks to the system guarantees it provides. Around 40% of the portfolio consists of hub-to-hub optical fibre and copper cable systems. The remaining 60%, consisting of components and systems in the field of connectivity and peripherals, is deployed primarily in the network hubs.

Turnover in the Telecom Solutions segment dropped 6.2% to € 156.8 million. This decline was largely due to a 27.8% drop in turnover from copper networks on the back of an accelerated shift towards optical fibre networks. This drop was offset somewhat by a 0.7% increase in turnover from optical fibre systems. The telecom sector has made investments in 4G networks a high priority, which has led to lagging investments in both copper networks and optical fibre networks.

EBITA was down by € 0.6 million. The ROS increased to 9.0%, from, 8.8% thanks to improved efficiency and the impact of lower raw materials prices.

Indoor telecom systems - home networking-systems, broadband connectivity, IPTV software solutions – turnover share 4.1%

Turnover was down slightly, by 2.3%. The decline was recorded in the second half of the year, due to the cut-back in turnover from the underperforming parts of the portfolio and reluctance among consumers in the Benelux region to invest in IT. The resultant drop in turnover was partly offset thanks to the priority put on upgrading broadband connections.

Fibre network systems - optical fibre, optical fibre cables, connectivity systems and components, active peripherals – turnover share 7.0%

Turnover showed a limited increase of 0.7%. Investments in 4G networks within Europe led to delays in investments in optical fibre networks in various countries. However, the previously announced investments and preparations for a large-scale roll-out of FttH (Fibre-to-the-Home) networks within Europe are still on the horizon. Optical fibre technology remains the technology of choice for a future-proof broadband network.

TKH developed new ideas to further reduce the costs per connection and the operational costs related to the network. One example was the introduction of robot systems based on vision technology in the optical fibre network hubs. This introduction progressed well and offers a good perspective to TKH’s international positioning.

Copper network systems – copper cable, connectivity systems and components, active peripherals – turnover share 2.0%

Turnover in this segment dropped by 27.8%. This decline in turnover was in line with the increased priority given to optical fibre networks and 4G networks and the ensuing shift in investments to these networks. The relevance of the copper network system activities is still extremely limited due to the sharp decline in turnover and TKH’s focus is therefore largely on supplying parts and maintenance for the existing networks.

Building Solutions

Profile

Building Solutions develops, produces and delivers solutions in the field of efficient electro- technical technology, ranging from applications within buildings to technical systems which, linked to software, provide efficiency solutions for the care and security sectors. TKH’s know-how in this segment is focused on vision technology and connectivity systems combined with efficiency solutions to reduce the throughput-time for the realisation of installations within buildings. In addition, TKH’s focus in this segment is on intelligent video, intercom and access monitoring systems for a number of specific sectors, including elderly care, parking, marine, oil & gas, tunnels and security for buildings and work sites.

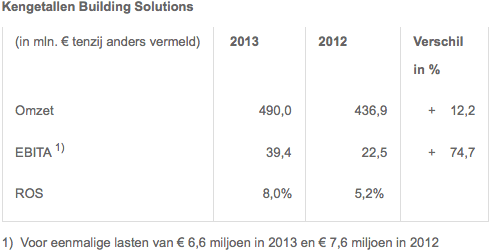

Turnover in the Building Solutions segment was up 12.2% at € 490.0 million. Acquisitions accounted for 10.9% of this growth, while organic growth came in at 2.7%. Reduced raw materials prices had a negative impact of 1.4% on turnover. Market conditions in the building and construction sector were challenging, which put pressure on margins in the connectivity segment in particular. The growth strategy in the selected vertical markets - care, marine - oil & gas, parking, tunnels and machine vision led to organic growth in the segment as a whole, despite a shrinking market in the building and construction sector.

EBITA increased to € 39.4 million, partly through acquisitions. Excluding acquisitions, EBITA was up 33.8% in line with the efficiency programmes we launched in 2012 and the growth we realised. In the fourth quarter of 2013, TKH decided to introduce an additional efficiency improvement programme. EBITA in the second half of the year was clearly higher than in the first half. The margin pressure in the connectivity segment had a negative impact on the programmes aimed at efficiency and margin improvements. The ROS nonetheless increased to 8.0% in 2013, from 5.2% in 2012.

Building technologies – energy-saving light and light switch systems, energy management systems, care systems, structured cabling systems – turnover share 7.3%

Turnover dropped by 5.9%, primarily as a result of a reluctance to invest in the building and construction sector. Growth was booked in the healthcare sector due to the fact that TKH’s technology is an effective response to the growing demand for efficiency solutions in this sector. The VieDome video communications platform, aimed at supporting remote healthcare, and the vision-technology-based system for the blister packaging and distribution of medications give TKH a solid position in this sector. The reduced construction volume led to a decline of more than 15% in the data networks market, which resulted in a drop in TKH’s turnover in the field of structured data networks. Turnover from energy-saving lighting systems for underground parking garages continued to increase on the back of the trend among clients to reduce their CO2 footprint. The combination of guiding and lighting technology puts TKH in a unique proposition in this field.

Vision & Security systems – Vision technology, systems for CCTV, video/audio analysis and detection, intercom, access control and registration, central control room integration – turnover share 19.5%

Turnover in this segment came in 32.4% higher. The acquisition of Augusta made a major contribution to this growth in turnover. Turnover increased 4.0% organically, as growth came under pressure from the reluctance to invest in the building and construction sector in the Benelux, as well as in traffic infrastructure.

Augusta’s results improved in the second half of the year, when compared to the first half, due to improved market conditions in the end-markets that are relevant to Augusta. The focus on the vertical growth markets introduced in late 2012 put the company in a successful position, especially in combination with demand from customers for integrated solutions. Our customers see considerable added value in the engineering expertise that enables us to come up with integrated systems, as well as our specific know-how of processes and the needs of end-users. TKH expanded its R&D capacity considerably to increase its technological lead.

Connectivity systems – specialty cable (systems) for shipping, rail, infrastructure, wind energy, as well as installation and energy cable for niche markets – turnover share 14.1%

Turnover increased by 3.6%, corrected for inventory reductions and reduced raw materials prices. This growth was largely realised outside the Benelux region. The reduced volume in the building and construction sector led to fierce competition and put pressure on margins. As a result, the growth in turnover combined with the efficiency improvement programmes that were launched have not yet resulted in the targeted return on sales. The growth in the second half of the year in our defined vertical markets and the alignment with the core technologies vision & security and communications did lead to a strong improvement in the results in the course of the year. We have decided to terminate the solar system activities completely due to the low returns.

Industrial Solutions

Profile

Industrial Solutions develops, produces and delivers solutions ranging from specialty cable, plug and play cable systems to integrated systems for the production of car and truck tyres. The company’s know-how in the automation of production processes and improvements in the reliability of production systems gives TKH the differentiating potential to respond to the increasing desire to outsource the construction of production systems or modules in a number of specialised industrial sectors, such as tyre manufacturing, robotics, medical and machine construction industries.

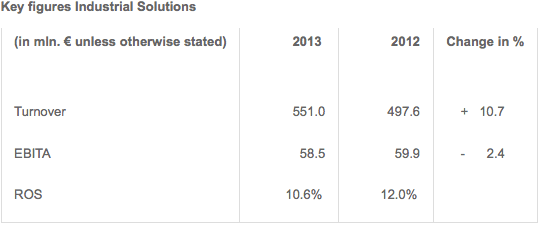

Turnover in the Industrial Solutions segment came in 10.7% higher at € 551 million. The acquisition of Augusta boosted turnover by 3.0%, while turnover increased by 9.1% organically. Raw materials prices had a negative impact of 1.4% on turnover. Manufacturing systems booked particularly strong turnover growth, while connectivity systems also recorded a slight increase in turnover. The second half of the year showed a clear improvement compared to the first half of the year, largely driven by improved market conditions in the industrial sector and TKH’s cutting edge technologies.

EBITA fell slightly by 2.4% to € 58.5 million, despite higher turnover. The major turnover contribution from new technology created an imbalance in the capacity utilisation at TKH’s various production facilities, which in turn led to higher than usual cost levels, partly on account of a major increase in the hiring of temporary staff in the Netherlands. Costs in the first half of 2013 were also higher due to capacity maintained in anticipation of expected growth and because of investments in new clients and new technologies. These investments translated into a stronger market position and record order intake.

Connectivity systems – specialty cable systems and modules for the medical, robot, automotive and machine building industries – turnover share 20.2%

Turnover came in 1.2% higher, corrected for a negative impact of 2.8% from lower raw materials prices charged on to customers. The first half of the year saw some reluctance in Europe to invest in capital goods, which resulted in a drop in turnover. This changed in the second half, resulting in organic growth of 12%. Investments increased in both the robotics sector and the medical sector. Positive developments in the German automotive sector also translated into a higher order intake among industry suppliers. We saw a continuation of the trend towards supplying complete systems to meet customers’ demands and this had a positive impact on our turnover growth.

Manufacturing systems – advanced manufacturing systems for the production of car and truck tyres, can washers, test equipment, product handling systems for the medical industry, machine operating systems – turnover share 25.8%

Turnover was up 19.5%, with 5.7% of this accounted for the acquired Augusta operations. Organic growth came in at 13.8%. The organic growth was largely due to improved market conditions for investments in capital goods. Order intake increased strongly from mid-2012 and in the second half of 2013 we booked record order intake of more than € 160 million in the tyre manufacturing segment. Our greatest success has been with the new technology launched since 2012, which was a major step forward in terms of the quality, productivity and flexibility of the manufacturing systems. This resulted in a further breakthrough in our position in the tyre manufacturing industry. We also saw a further strengthening of our position among the five major tyre manufacturers. The major share of turnover from new technologies did, however, create an imbalance in the capacity utilisation among our production facilities, which led to higher than usual costs and meant we were able to produce a smaller proportion of systems in Asia. Preparations were made for a further structural increase in our production capacity, both in Asia and in the Netherlands. We were able to meet demand thanks to a high number of temporary hires and the leasing of external facilities. This did result in some inefficiencies, which are likely to normalise again in the second half of 2014, thanks to the further expansion of our own production capacity.

Dividend proposal

At the Annual General Meeting to be held on 14 May 2014, TKH will propose the payment of a dividend of € 0.75 per (depositary receipt for a) share (2012: € 0.65). This amounts to a pay-out ratio of 50.7% of the net profit before amortisation and one-off income and expenses, and 76.5% of the net profit. TKH will propose the payment of an optional dividend in cash or in shares, which will be charged to the reserves. TKH will determine the dividend payment in shares one day after the end of the optional period on the basis of the average price of TKH shares during the last five trading days of the optional period, which shall end on 3 June 2014. The dividend will be payable, in cash or in shares, on 6 June 2014.

Appointment Supervisory Board members

During the General Meeting of Shareholders of TKH on 14 May 2014, Ms. M.E. Van Lier Lels and Mr. P. Morley MSc. will be stepping down as members of the Supervisory Board on the basis of the prevailing retirement scheme. Ms. Van Lier Lels is eligible for reappointment. Mr. Morley is not eligible for reappointment because the maximum period of three terms of four years has been reached.

The Supervisory Board has decided to nominate Ms. Van Lier Lels for reappointment. In addition the Supervisory Board nominates for appointment as new member of the Supervisory Board Mr. Antoon De Proft, CEO of IMEC (European research centre in Leuven – Belgium), CEO of Quest For Growth, board member of Barco and former CEO of ICOS Vision Systems. Mr. De Proft has the Belgian nationality.

Outlook

The market conditions are volatile in the segments in which TKH operates. On the one hand, the global economic situation is showing signs of improvement in a number of market segments compared with last year. On the other hand, the general economic situation is still fragile, as market developments, especially in Asia, are still uncertain.

Within Telecom Solutions, following the realisation of investments in 4G networks, the investments in optical fibre networks will again increase. Due to the current overcapacity at a number of manufacturers of optical fibre, margins will remain under a certain amount of pressure in the first half of 2014, in line with margin development in the second half of 2013.

At Building Solutions, we expect to see a continued drop in investments in the building and construction sector, and the market conditions will continue to be challenging. On the other hand, we could see growth in a number of the vertical markets TKH is focusing on, thanks to TKH’s trend-setting core technologies and the positive trends with regard to investments in these markets.

At Industrial Solutions, in 2013, we saw a strong increase in order intake in the sub-segment manufacturing systems. There are also signs that investments in the industrial sector will be higher in 2014 compared with last year. If the order intake develops positively in the course of the year, we could see an increase in profit.

In view of the continued economic uncertainty in a number of segments, it is too early to give a full-year 2014 profit forecast for the entire TKH group. As usual, TKH will aim to give a profit forecast for the full year at the presentation of its first-half results in August 2014.

The complete press release can be downloaded in PDF